Accounting is the process of recording, classifying, and summarizing financial transactions. It helps businesses keep track of their money and make informed decisions. It is used to check the financial position of the business. Every transaction in accounting affects two accounts one is debited and the other is credited.

For example: Paid rent affects two accounts, in debit the entry will be rent and in credit the entry will be cash because there is outflow of cash.

To understand this clearly, we need to learn about types of accounts and the golden rules of accounting.

What are Golden Rules of Accounting?

The Golden Rules of Accounting govern how debit and credit entries are recorded in the accounting system. In simple terms, debits and credits are used to reflect the movement of value in a transaction.

- Debit refers to an entry that increases assets or expenses and decreases liabilities or income. When a business acquires an asset or incurs an expense, the respective account is debited.

- Credit, on the other hand, is used to record a decrease in assets or expenses and an increase in liabilities or income. When a business sells an asset or earns income, the respective account is credited.

Each transaction involves both a debit and a credit entry, which must always balance, ensuring that the accounting equation remains in equilibrium. The golden rules ensure consistency in the application of debits and credits, helping to maintain accurate and balanced financial records.

Types of Accounts with their Golden Rules & Examples

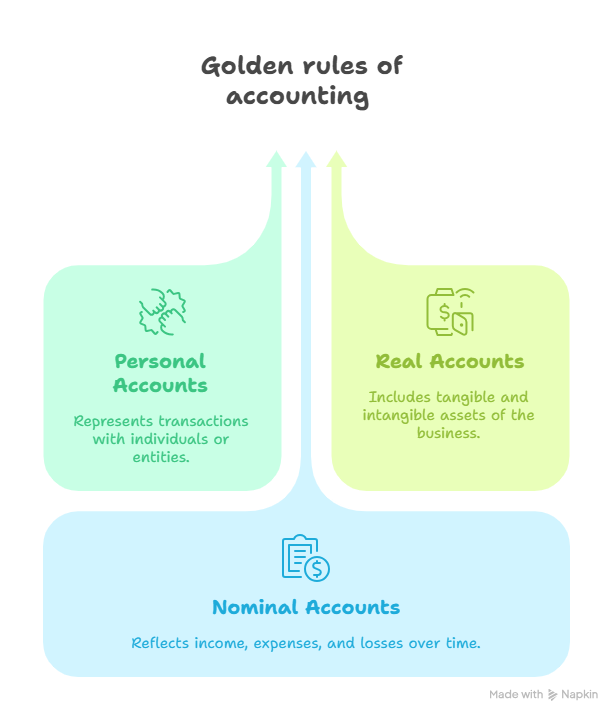

The Golden Rules help you decide what to debit and what to credit in any financial transaction. These rules are based on the three types of accounts used in accounting: Personal, Real, and Nominal accounts.

1. Personal Account

Personal account is a type of account that is related to individuals, companies, or organizations. A personal account keeps a record of how much someone owes you or how much you owe them.

Rule: Debit the receiver, Credit the giver.

Example: You pay ₹1,000 to Ramesh.

→ Ramesh’s account (Personal) is credited.

→ Cash is debited.

2. Real Account

A Real Account is an account that records all the tangible as well as intangible assets and liabilities of a business. These can be things like cash, furniture, buildings, land, machinery, vehicles, goodwill, patents.

Rule: Debit what comes in, Credit what goes out.

Example: You buy furniture for cash.

→ Furniture (asset) comes in → Debit

→ Cash goes out → Credit

3. Nominal Account

A Nominal Account is an account that records all the expenses, losses, incomes, and gains of a business. It tell us how much profit business made at the end of the financial year.

Rule: Debit all expenses and losses, Credit all incomes and gains.

Example: You pay ₹2,000 as salary

→ Salary is an expense → Debit

→ Cash goes out → Credit

Benefits of Golden Rules of Accounting

The Golden Rules of Accounting help you know how both accounting side effects like what to debit and what to credit in every financial transaction.

- Makes bookkeeping simple and reduce errors and mistakes. Great for small businesses to manage their accounts properly, so everyone can understand the basic accounting concepts.

- Helps in understanding financial statements i.e. Income statement, balance sheet and cash flow statement also helpful to understand basic accounting- journal entries, ledgers, and trial balances.

- Useful for students, accountants, and business owners to check the actual financial position of the business whether the company or business was in profit or loss so the owner or accountant make accurate decisions

- Builds a strong foundation for learning the advanced accounting transactions. It ensures every transaction is recorded Builds a strong foundation for learning the advanced accounting transactions, It ensures every transaction is recorded correctly as debit and credit.

Conclusion

Understanding the types of accounts and golden rules of accounting is the first step in learning how businesses manage their money. Whether you stick with the traditional approach or use modern rules, the basic goal remains the same to record every transaction accurately and clearly and it is useful to check the actual financial position of the business like whether the business was in profit or loss.

Golden rules of accounting help you to understand the basic accounting concepts.

FAQs

1. What is accounting ?

Accounting is the process of keeping financial records of all the money a business earns and spend to make accurate decisions.

2. What is the difference between real and nominal accounts?

Real accounts are related to tangible and intangible assets. Nominal accounts records the transaction related to expenses and incomes.

3. Why do we follow the golden rules?

It is the basic accounting concepts that help you to understand the financial position of the business. They help us know which account will be debited and which account will be credited in a transaction.

4. Is modern accounting better than traditional accounting?

Modern rules align with today’s software systems and financial practices, and traditional accounting helpful to understand the basic accounting concepts but both are useful.

5. What is an asset account?

An asset account that shows what the business owns, like cash, buildings, or equipment. It records both tangible and intangible assets.

6. Can I learn accounting without being a commerce student?

Yes! Accounting basics are simple and anyone can learn them with interest and practice. And if you understand the basic golden rules of accounting then it will be helpful for you to understand.

7. What is the Accounting Cycle?

The accounting cycle is the step-by-step process of recording, summarizing, and reporting a business’s financial transactions.

Steps in the Accounting Cycle:

- Identify transactions

- Record journal entries

- Post to ledger

- Prepare trial balance

- Make adjustments

- Prepare financial statements

- Close the books

8. What is a Ledger Book?

A ledger book is a book or software where all the financial transactions of a business are recorded in a classified manner to make accurate decisions.

9. Difference Between Debit and Credit?

| Feature | Debit | Credit |

|---|---|---|

| Meaning | Entry on the left side | Entry on the right side |

| Used When | Asset/Expense increases | Liability/Income increases |

| Also Used When | Liability/Income decreases | Asset/Expense decreases |

| Example | Buying furniture (Asset ↑) Debit. | Earning revenue (Income ↑) Credit. |

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}